“We skipped Goa again this year. The kids were disappointed. But did we make the right call?”

If you’ve had that conversation — or just in your head — you’re not alone. Every summer, millions of Indian families wrestle with the same question: Do we travel and make memories, or do we stay disciplined and build wealth?

The good news? It doesn’t have to be either-or.

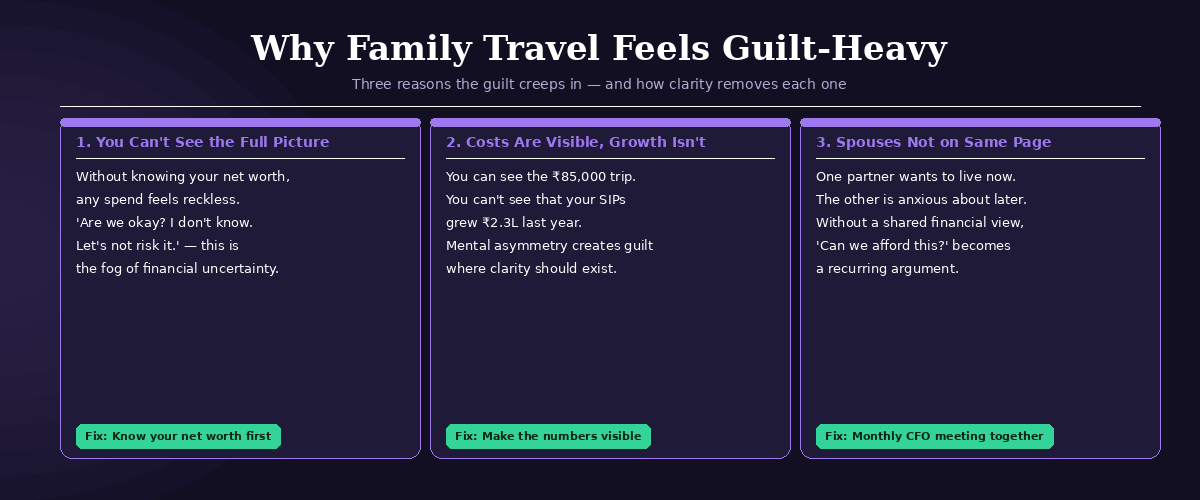

Why Family Travel Feels Guilt-Heavy

1. You Can’t See Your Full Financial Picture

If you don’t know exactly what your family’s net worth is, any spend feels reckless. “Are we okay? I don’t know. Let’s not risk it.” This is the fog of financial uncertainty — and it makes everything feel more expensive than it is.

2. Travel Costs Are Visible; Compound Growth Isn’t

You can see the ₹85,000 you spent on a Manali trip. You can’t easily see that your SIPs grew ₹2.3 lakh last year. The mental asymmetry creates guilt where clarity would create confidence.

3. You and Your Spouse Might Not Be on the Same Page

One partner wants to experience life now. The other is anxious about the future. Without a shared financial view, “Can we afford this?” becomes a recurring argument rather than a five-minute data check.

The False Choice We’ve All Been Sold

Somewhere along the way, personal finance content decided that spending on experiences is the enemy of financial independence. “Every rupee you spend on a vacation is a rupee not compounding in your SIP.”

Technically true. Emotionally bankrupt.

Families aren’t spreadsheets. Children grow up. Summers don’t repeat. And the best financial plan is one your family will actually stick to — not one that makes everyone miserable.

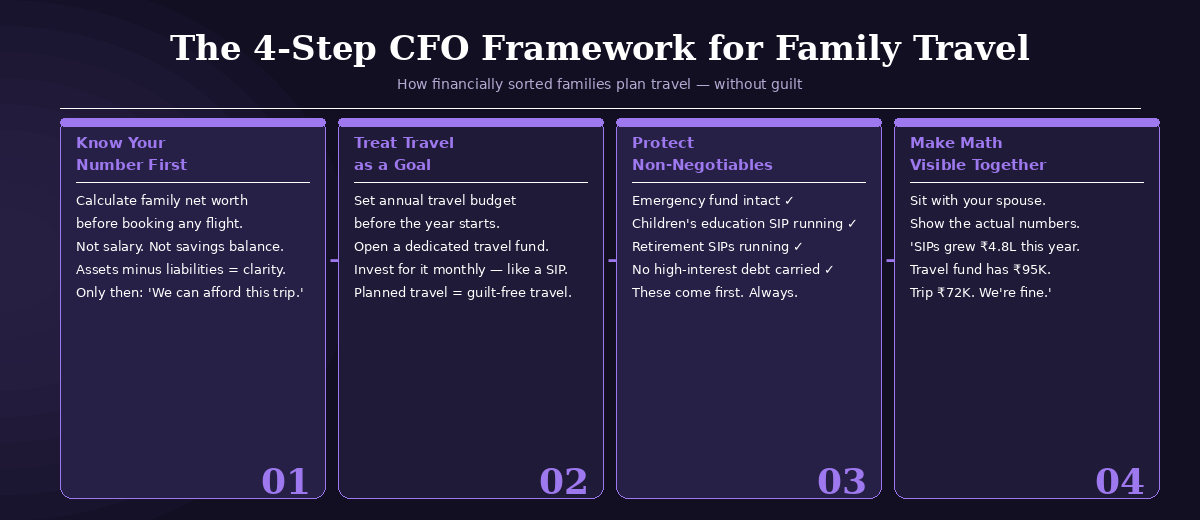

The Framework: Budget for Travel Like a CFO

Step 1: Know Your Number First

Before booking a single flight, know your family’s current net worth. Not your salary. Not your savings account balance. Your net worth — assets minus liabilities. Add up your bank accounts, SIPs, FDs, and loans. See what’s growing, what’s due, and what’s sitting idle.

Only from this position can you confidently say: “We can afford ₹1.2 lakh on this trip and still hit our goals.”

Step 2: Treat Travel as a Goal, Not a Splurge

Every year, decide your travel budget before the year starts — proactively — and invest for it. The table below gives you a starting point based on income.

Step 3: Protect Your Non-Negotiables First

- Emergency fund (3–6 months of expenses, liquid)

- Children’s education goal on track

- Retirement SIPs running as planned

- No high-interest debt being carried over

Once these are protected, the travel budget is genuinely guilt-free.

Step 4: Make the Math Visible to Both Partners

Sit down with your spouse and actually show the numbers.

“Our net worth has grown ₹4.8 lakh this year. Our travel fund has ₹95,000 in it. The Shimla trip costs ₹72,000 all-in. We’re fine.”

Smart Travel Budgeting Tips for Indian Families

- Book Early, Save Big: Flights booked 6–8 weeks out can save 30–40%.

- Off-Peak Within Peak: Travel first week of May or last week of June to save 20–30%.

- Domestic Over International: India has extraordinary destinations at a fraction of the cost.

- Split the Trip: Consider shorter frequent trips over one expensive one.

- Use Points and Miles: Credit card rewards can often cover a full trip every 2 years.

The Compound Effect of Family Memories

Children who travel develop curiosity, adaptability, and cultural empathy. These are life skills that no FD can create.

Stop treating vacations as financial crimes. Plan smart. Know your numbers. Set the goal. Fund it. Go.

This blog is for informational purposes only and does not constitute financial advice. Famli is a SEBI-registered Investment Adviser (INA000021979). All figures and guidelines used in this article are illustrative only. Consult a qualified financial planner for personalised advice.