Appraisal season is here. The email’s landed. Your salary is going up.

For most working professionals in India, this is the one moment in the year where income actually jumps. And what happens next usually follows a predictable script: a celebratory dinner, a new phone, maybe a slightly bigger EMI on a car upgrade. A month later, the hike has quietly dissolved into “lifestyle.”

Sound familiar?

Here’s the thing: your appraisal isn’t just a reward for last year’s work. It’s a rare, built-in opportunity to change your financial future, without changing how you live today. The key? Redirecting a meaningful portion of that hike into SIPs before your spending habits catch up.

Let’s break down exactly how much, and how to think about it.

India’s Salary Hike Landscape in 2026

Before we talk allocation, let’s set some context.

According to multiple industry reports, the average salary hike across India Inc in 2026 is projected at around 9%. Sectors like pharmaceuticals, manufacturing, and real estate are expected to go slightly higher (9.5 to 10.2%), while IT services may see more modest increases in the 7 to 9% range.

What’s also interesting: real wage growth, after adjusting for inflation, has averaged just 0.4% annually over the past decade. That means most of your hike is simply keeping pace with rising costs, not making you meaningfully wealthier.

This is precisely why how you allocate your hike matters more than the hike itself.

The “Lifestyle Creep” Trap

There’s a well-documented behaviour in personal finance called lifestyle inflation (or lifestyle creep). Every time your income goes up, your spending quietly rises to match it. Bigger apartment, better restaurants, premium subscriptions, a few more “treats” each month.

None of these are bad in isolation. But compounded over 10 to 15 years of annual hikes, lifestyle creep is the single biggest reason why people who earn well still don’t feel financially secure.

The antidote? A decision rule. Before you adjust your lifestyle, adjust your investments.

The Half-First Rule: A Framework for Your Salary Hike

Most budgeting advice tells you how to split your entire salary. But your hike is different. It’s new money, money you weren’t spending last month, which means you have a clean window to direct it before habits form around it.

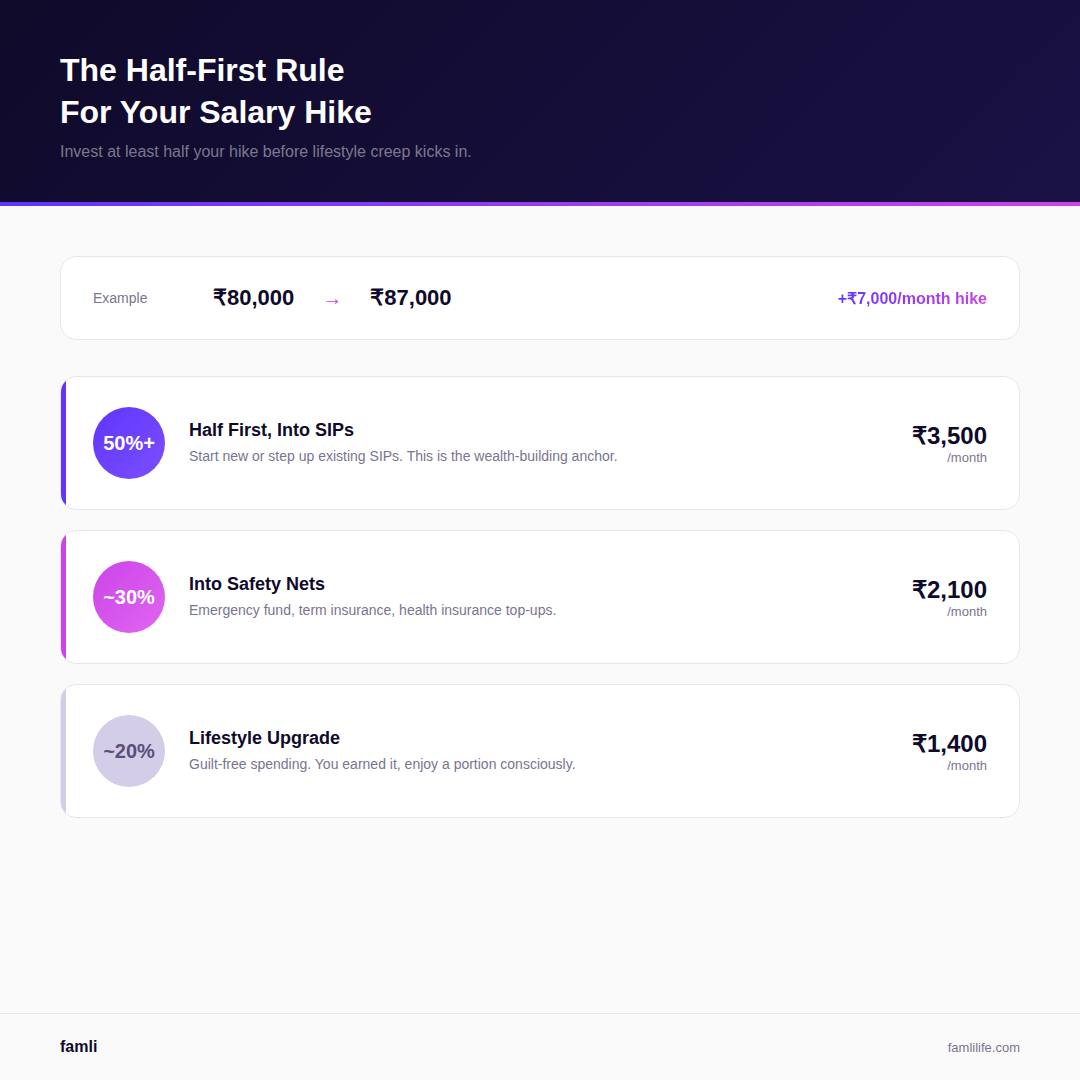

Here’s a simple framework we call the Half-First Rule: invest at least half your hike before you do anything else with it.

At least 50% of your hike: into SIPs (or step up existing SIPs)

This is the non-negotiable anchor. Half your raise goes directly into investments. If your monthly salary went up by Rs 10,000, that’s Rs 5,000 into new or topped-up SIPs. Why half? Because it’s large enough to make a real difference over 10 to 15 years of compounding, but not so aggressive that you’ll feel squeezed and abandon the plan.

About 30% of your hike: into financial safety nets

This includes topping up your emergency fund, increasing your term insurance cover if needed, or boosting your health insurance. These aren’t exciting, but they’re the foundation that keeps your SIPs running even when life throws surprises. If your safety nets are already solid (6 months’ expenses saved, adequate insurance), you can shift this portion into SIPs too.

The remaining 20%: enjoy it

Yes, spend some of it. Upgrade something. Eat somewhere nice. The point isn’t deprivation. It’s making sure the “enjoy” portion is a conscious decision, not an unconscious default that swallows the entire hike.

A Quick Example

Let’s say your monthly take-home goes from Rs 80,000 to Rs 87,000 after a 9% hike. That’s a Rs 7,000 monthly increase.

| Allocation | Amount | What It Does |

|---|---|---|

| Half into SIPs | Rs 3,500/month | Compounds over time, builds wealth |

| 30% into safety nets | Rs 2,100/month | Tops up emergency fund or insurance |

| 20% lifestyle upgrade | Rs 1,400/month | Guilt-free spending |

This way, you’re building wealth, staying protected, and still enjoying your raise. No sacrifice required.

Why Step-Up SIPs Are the Real Power Move

Most people set up their SIPs once and forget them. That’s disciplined, yes. But it also means your investments stay flat while your income keeps growing.

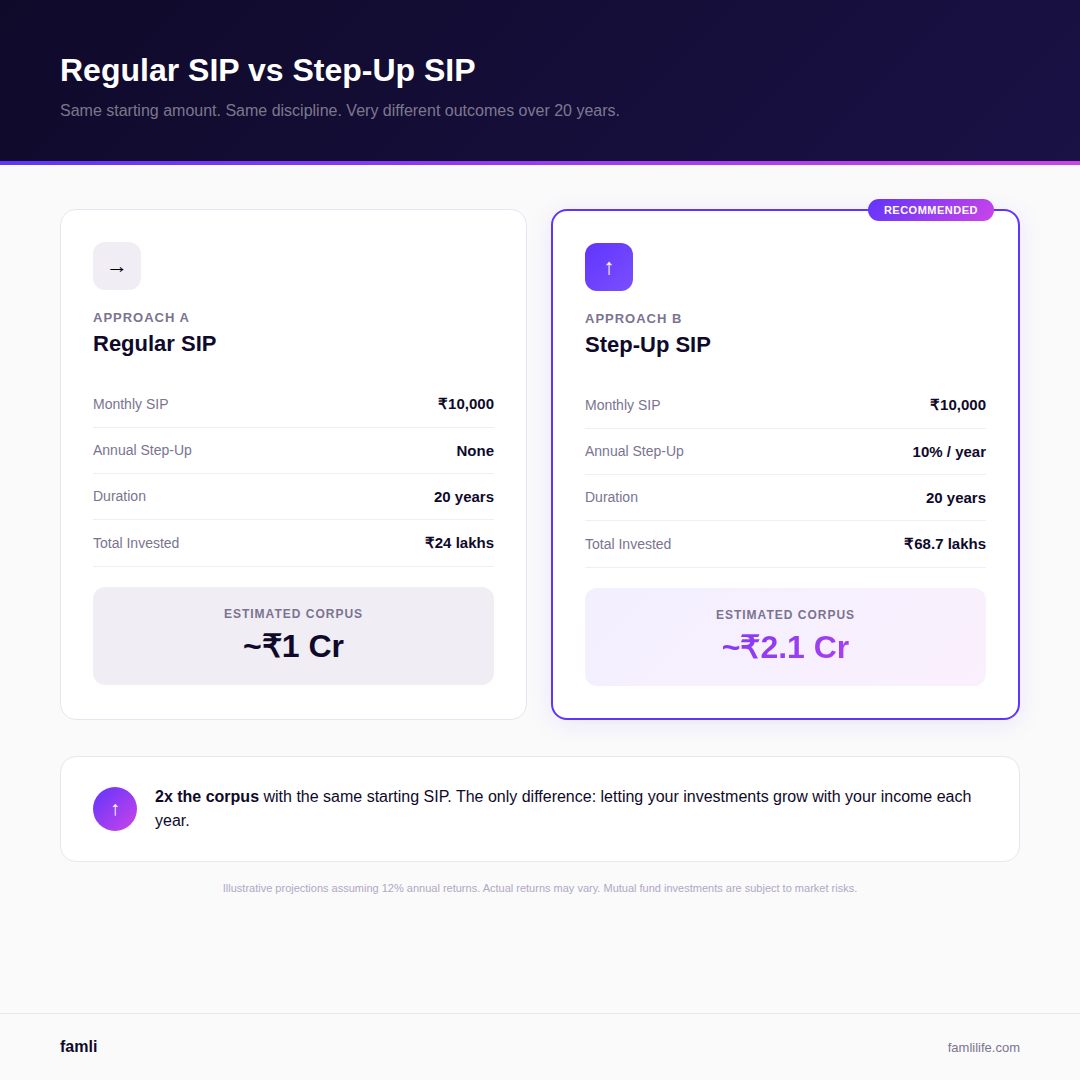

Enter the step-up SIP (also called a top-up SIP). This is a feature offered by most mutual fund platforms where your SIP amount automatically increases by a fixed percentage or a fixed amount every year.

Here’s why it matters:

The compounding difference is massive. If you invest Rs 10,000 per month in a regular SIP for 20 years at 12% returns, you’d end up with roughly Rs 1 crore. But if you step up that SIP by just 10% every year (matching a typical salary hike), your corpus jumps to over Rs 2 crore. Same starting point. Same discipline. Double the outcome, just because you let your investments grow with your income.

You don’t feel the pinch. Because you’re only increasing your SIP by a fraction of your hike, your day-to-day spending doesn’t change. The increase is absorbed before you even notice it.

It naturally fights inflation. A fixed Rs 10,000 SIP today will feel like Rs 5,000 in purchasing power 15 years from now. Stepping up keeps your real investment amount meaningful.

The Right Step-Up Rate: A Simple Framework

A common question is: how much should I step up my SIP by each year?

Here’s a practical framework:

Conservative (5% step-up): Good if your income growth is unpredictable or you have significant EMIs. Keeps the increase manageable.

Moderate (8 to 10% step-up): Ideal for most salaried professionals. Roughly matches the average salary increment and absorbs a meaningful chunk of each raise.

Aggressive (15%+ step-up): Suitable if you’re in your 20s with minimal fixed expenses, or if you’re playing catch-up on investments after a late start.

A useful rule of thumb: if your salary grows by 9%, try to step up your SIPs by 5 to 8%. This ensures you’re investing more each year while still allowing your lifestyle to improve gradually.

What Most People Get Wrong

Mistake 1: Waiting for a “better time” to invest the hike. The best time to redirect your hike into SIPs is the same month your new salary kicks in. Before you adjust to the higher number. Delay it by even two months, and the money will find somewhere else to go.

Mistake 2: Stopping SIPs during market dips. Market corrections are actually when your SIP works hardest, buying more units at lower prices. A hike-funded SIP that runs through volatility is far more powerful than one that gets paused at the first red screen.

Mistake 3: Ignoring the basics before stepping up. Before increasing your SIPs, make sure you have at least 3 to 6 months of expenses in an emergency fund, adequate health insurance, and a term life cover if you have dependents. SIPs build wealth; insurance protects it.

Mistake 4: Over-committing and then breaking the SIP. Don’t put 100% of your hike into SIPs if that means you’ll stop them six months later. A sustainable SIP that runs for 15 years beats an aggressive one that lasts 15 months.

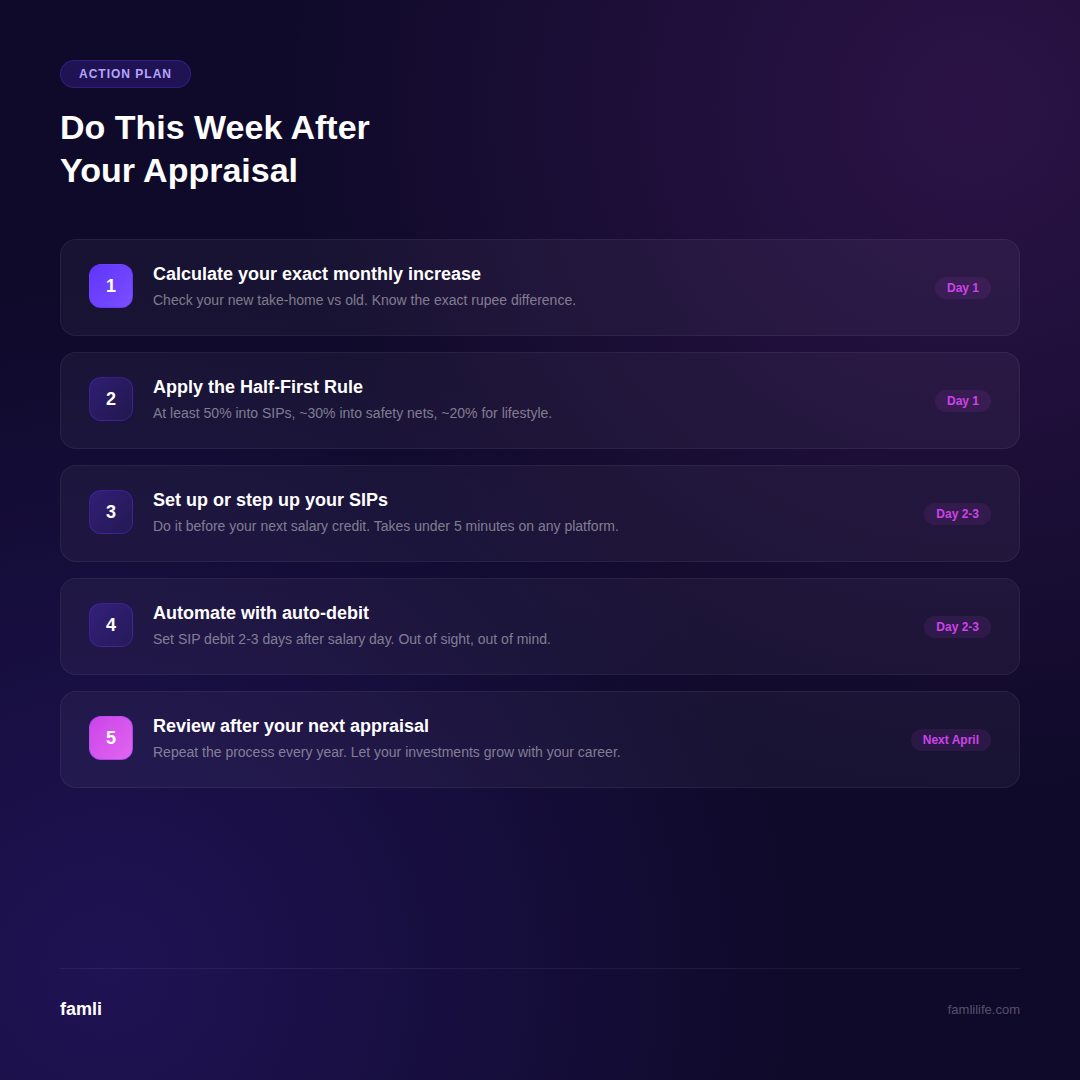

A Practical Action Plan (Do This Week)

Here’s what to do right after your appraisal:

Step 1: Calculate the exact monthly increase in your take-home salary.

Step 2: Apply the Half-First Rule. Commit at least half to SIPs, allocate the rest between safety nets and lifestyle.

Step 3: Set up or step up your SIPs before the next salary credit date. Most platforms (Groww, Kuvera, Coin by Zerodha) let you do this in under 5 minutes.

Step 4: Automate it. Set up auto-debit so the SIP runs two to three days after your salary hits your account. Out of sight, out of mind.

Step 5: Review once a year, right after your next appraisal. Repeat the process.

The Bigger Picture

Here’s what consistent step-up SIPs can look like over time:

| Scenario | Monthly SIP | Annual Step-Up | Duration | Estimated Corpus (at 12%) |

|---|---|---|---|---|

| Just starting out | Rs 5,000 | 10% | 20 years | ~Rs 1.06 crore |

| Mid-career boost | Rs 15,000 | 8% | 15 years | ~Rs 1.12 crore |

| Aggressive saver | Rs 25,000 | 10% | 15 years | ~Rs 1.87 crore |

These are illustrative projections assuming 12% annual returns. Actual returns may vary. Mutual fund investments are subject to market risks. Please read all scheme-related documents carefully before investing.

The numbers are striking. A person starting with Rs 5,000 per month and consistently stepping up by 10% can build a corpus comparable to someone investing Rs 15,000 per month with a lower step-up. Starting amount matters, but consistency and annual increases matter more.

Your Appraisal Is a Financial Turning Point

Every year, your employer gives you a raise. But whether that raise actually changes your financial life depends entirely on what you do in the first 48 hours after the number lands.

The simplest decision you can make: before upgrading anything else, upgrade your SIPs.

It doesn’t require a financial advisor. It doesn’t require complex calculations. It requires one decision, one auto-debit setup, and the discipline to repeat it every year.

Your future self will thank you.

Investments are subject to market risks. Famli is a SEBI-registered Investment Adviser (INA000021979). Registration does not guarantee performance of advice or assurance of returns. Please read all scheme-related documents carefully before investing.

Track your complete financial picture with Famli. See how your SIPs, FDs, and every other asset fit into your family’s net worth, all in one place. Download Famli