The 50/30/20 rule is one of the most popular personal finance frameworks in the world.

Except it was not built for you.

It was not built for a single earner in Pune or Bengaluru who is paying a home loan EMI, running a household of five, sending Rs 15,000 a month to aging parents in another city, and trying to build a corpus for their child’s engineering seat all at the same time.

The 50/30/20 rule is a framework. And like any framework, it needs to be adapted to the reality it is being applied to. This article does exactly that. It breaks down how the rule shifts for the modern Indian joint family, what happens to your budget when aging parents enter the picture, and how to protect your savings bucket even when everything else is pulling at it.

What Is the 50/30/20 Rule?

The 50/30/20 rule is a budgeting method popularised by US Senator Elizabeth Warren in her book All Your Worth. The idea is simple: divide your after-tax income into three categories.

- 50% for Needs: rent or home loan EMI, groceries, utilities, insurance, transport, minimum debt repayments

- 30% for Wants: dining out, subscriptions, travel, entertainment, clothes, hobbies

- 20% for Savings and Investments: emergency fund, SIPs, FD contributions, NPS, PPF, retirement corpus

The 50/30/20 rule divides your monthly take-home income into three parts: 50% for essential needs, 30% for lifestyle wants, and 20% for savings and investments. It is a starting point for budgeting, not a rigid prescription.

Why the Standard 50/30/20 Rule Does Not Work for Indian Families

The original framework assumes a few things that simply do not hold true for most Indian households.

- It assumes you are budgeting for yourself, not a family system with shared obligations.

- It assumes your “needs” are predictable. Indian families often carry variable obligations: a parent’s medical bill, a sibling’s exam fee, a relative’s wedding contribution.

- It does not account for elder care, which is not a “want” but is also not a standard bill. It sits somewhere in between and often swells unexpectedly.

- It assumes your wants are optional. But for Indian professionals, many “wants” carry social expectations. A family holiday is not purely discretionary when it is the only time aging parents get to see grandchildren.

- It was designed for a country where childcare, elder care, and education are heavily institutionalised and expensive. In India, these are often family-borne costs.

The result? If you try to apply the standard rule to an Indian joint family budget, your Needs category alone frequently exceeds 60 to 70% of take-home pay which leaves you choosing between wants and savings every single month.

The 50/30/20 Rule Adapted for the Indian Single-Earner Joint Family

The adapted version does not throw out the framework. It redefines the categories to reflect Indian financial reality. Here is the core principle shift:

| The Indian Adaptation Principle In the Indian context, “Needs” must include shared family obligations. “Wants” must be ruthlessly prioritised. And “Savings” must be protected as a non-negotiable line item before you even look at discretionary spending. |

This means the percentages shift depending on your family situation. The table below shows how the allocation changes across three common household types.

Table 1: How the 50/30/20 Rule Shifts for Indian Family Types

| Budget Category | Standard Rule (Western / Nuclear) | Urban Nuclear Indian Family | Single Earner + Aging Parents | Single Earner + Parents + Children’s Education |

| Needs (Housing, Food, Utilities, Insurance, Transport) | 50% | 55% | 62% | 67% |

| Wants (Lifestyle, Dining, Travel, Entertainment) | 30% | 20% | 13% | 8% |

| Savings & Investments (SIPs, FDs, NPS, Emergency Fund) | 20% | 25% | 25% | 25% |

| Aging Parent Support (included in Needs above) | N/A | 0% | 8 to 12% | 8 to 12% |

| Children’s Education (included in Needs above) | N/A | 5% | 5% | 10 to 15% |

Note: Figures are illustrative based on a monthly take-home income of Rs 1,00,000. Actual allocations will vary based on city, income level, and family composition. The 25% savings target is a floor, not a ceiling.

Breaking Down the “Needs” Bucket for Indian Families

The needs bucket in an Indian family budget carries significantly more than the Western definition suggests. Here is what should legitimately sit in your 50 to 67% needs category.

Standard Needs (apply to all household types)

- Home loan EMI or rent

- Household groceries and cooking expenses

- Utility bills: electricity, water, gas, internet, mobile plans

- Health insurance premiums for the entire family (including parents)

- Vehicle EMI and fuel or public transport

- Minimum repayments on any outstanding personal loan or credit card

- Term life insurance premium

Indian Family Additions to Needs

- Monthly transfer to aging parents: If parents are dependent on you, this is a need, not a want. Treat it like an EMI.

- Parents’ health insurance or top-up plan: Senior citizen premiums are steep. Budget Rs 15,000 to Rs 30,000 per year depending on age and pre-existing conditions.

- Children’s school fees: Monthly tuition, transport, activity fees. This belongs in needs, not wants.

- Domestic help: In a dual-obligation household, this is infrastructure, not luxury.

- Occasional medical emergencies for parents: Build a small monthly provision of Rs 3,000 to Rs 5,000 for this. Otherwise one specialist visit destroys your budget.

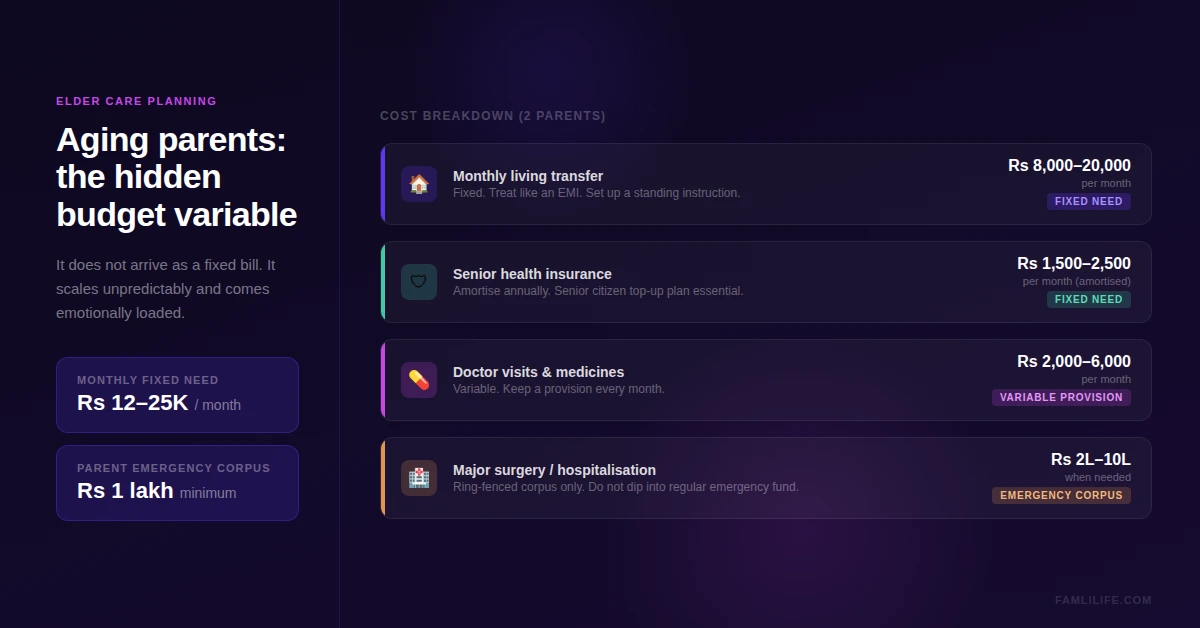

Aging Parents and Elder Care: The Hidden Budget Variable

Of all the budget pressures on Indian single earners, aging parent support is the least discussed and the most disruptive. It does not arrive as a fixed bill. It arrives suddenly, scales unpredictably, and comes emotionally loaded.

Here is how to plan for it properly.

The Elder Care Cost Framework for Indian Families

| Cost Type | Monthly Estimate (2 parents) | Where It Goes in Budget | Planning Strategy |

| Regular monthly transfer (living expenses) | Rs 8,000 to Rs 20,000 | Needs (fixed) | Treat as a fixed EMI. Set up a standing instruction. |

| Health insurance premium | Rs 1,500 to Rs 2,500/month amortised | Needs (fixed) | Buy a senior citizen top-up. Include in annual budgeting. |

| Ad hoc medical: doctor visits, medicines | Rs 2,000 to Rs 6,000 | Needs (variable provision) | Keep a Rs 50,000 to Rs 1,00,000 parent medical fund as part of emergency corpus. |

| Major medical: surgery, hospitalisation | Rs 0 (most months), Rs 2L to Rs 10L (when needed) | Emergency fund draw | Critical illness cover + separate corpus. Do not rely on health insurance alone. |

| Visits and travel to parents’ city | Rs 0 to Rs 5,000/month amortised | Wants (but socially essential) | Budget Rs 30,000 to Rs 50,000 annually for this. Split from discretionary. |

| Home modifications for elderly parents | One-time: Rs 30,000 to Rs 2,00,000 | Planned outflow | Treat as a goal in your financial plan. Not a surprise expense. |

The single most important thing you can do for elder care planning is to separate the predictable from the unpredictable. Monthly transfers and premiums go in your budget. Medical emergencies go in a ring-fenced corpus that you do not touch for anything else.

| How Much Should I Budget for Aging Parents in India? For a single earner supporting two aging parents in India, budget Rs 12,000 to Rs 25,000 per month as a fixed need. Additionally, maintain a separate parent emergency corpus of at least Rs 1,00,000 that you do not use for anything else. This should sit outside your regular emergency fund. |

Children’s Education as a Fixed Expense, Not a Variable

Most Indian parents instinctively treat children’s education costs as a need. But the way it is planned for makes all the difference.

The problem is that education expenses come in two forms: the current cost (school fees, tuition, books) and the future cost (college, engineering, medicine, MBA). Families that only budget for the current cost find themselves scrambling for the future cost.

Current Education Costs: Goes in the Needs Bucket

- School fees (annual, amortised monthly)

- School transport

- Tuition and coaching classes

- Books, stationery, uniforms

- School activity and exam fees

For a child in a mid-range private school in an Indian metro, this typically runs Rs 8,000 to Rs 20,000 per month. Treat this as a fixed need in your budget.

Future Education Costs: Goes in the Savings Bucket

The 20% savings allocation must include a dedicated education goal SIP. This is one of the most critical uses of the savings bucket for Indian families with children under 12.

| Child’s Current Age | Years Until College | Target Corpus (Engineering/General Degree) | Required Monthly SIP (at 12% CAGR, illustrative) |

| 2 years | 16 years | Rs 30,00,000 | Rs 3,200/month |

| 5 years | 13 years | Rs 30,00,000 | Rs 5,100/month |

| 8 years | 10 years | Rs 30,00,000 | Rs 8,600/month |

| 10 years | 8 years | Rs 30,00,000 | Rs 13,200/month |

| 12 years | 6 years | Rs 30,00,000 | Rs 21,000/month |

Important: The SIP returns above are purely illustrative and based on a 12% CAGR assumption. Actual mutual fund returns vary and are not guaranteed. The purpose is to show how urgently the monthly SIP requirement grows as you delay starting.

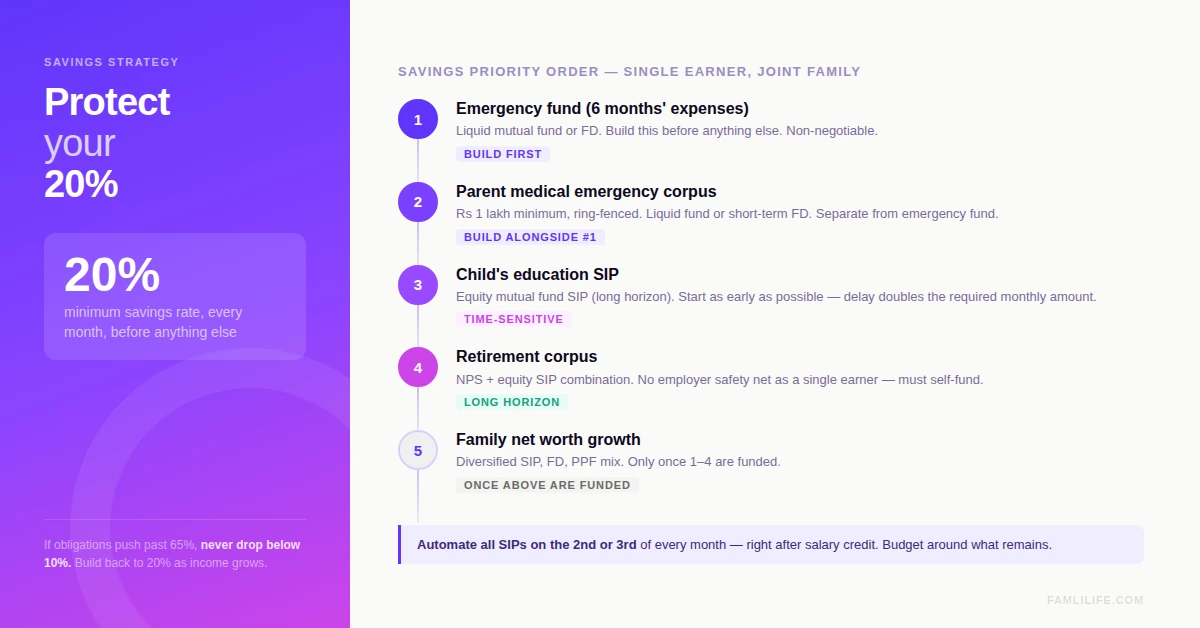

SIPs and the 20% Savings Rule: Making It Stick When Life Is Pulling It Apart

The most common mistake Indian single earners make is treating the savings bucket as what is left over after everything else. It is not. It is the first thing that leaves your account, every month, before you decide what you want or need.

This is the principle behind SIPs (Systematic Investment Plans). You commit a fixed amount. It goes out on the 1st of the month. You budget around what remains.

How to Protect Your 20% When Obligations Are High

| Savings Goal | Who It Is For | Recommended Vehicle | Priority |

| Emergency Fund (6 months’ expenses) | Everyone | Liquid mutual fund or FD | 1 (build this first) |

| Parent Medical Emergency Corpus | Anyone with dependent parents | Liquid fund or short-term FD | 2 (build alongside emergency fund) |

| Child’s Education Corpus | Parents with children under 14 | Equity mutual fund SIP (long horizon) | 3 |

| Retirement Corpus | Single earner (no corporate safety net) | NPS + Equity SIP combination | 4 |

| Family Net Worth Growth | All family members together | Diversified SIP + FD + PPF mix | 5 (once above are funded) |

If your needs genuinely push past 65% of take-home, your savings percentage may temporarily drop below 20%. That is okay. But never let it drop below 10%. And make a plan to build it back up as income grows or expenses reduce.

| How Should a Single Earner Prioritise Savings in India? For a single earner supporting a family, prioritise savings in this order: emergency fund first, parent medical corpus second, child’s education SIP third, and retirement via NPS or equity SIPs fourth. Automate all of them via standing instructions so they leave your account before you can spend them. |

The Master Reference Table: 50/30/20 Adapted Across Indian Life Stages

Use this table to find the adapted allocation closest to your current life situation.

| Life Situation | Suggested Needs % | Suggested Wants % | Suggested Savings % | Key Budget Priority |

| Young professional, no dependents, renting | 45% | 30% | 25% | Build emergency fund fast. Start SIP early. |

| Couple, no children, own home (EMI) | 52% | 23% | 25% | Protect the savings rate. Avoid lifestyle inflation. |

| Couple + 1 child, school age | 58% | 17% | 25% | Start education SIP immediately. |

| Single earner + aging parents (city) | 62% | 13% | 25% | Build parent medical corpus alongside SIPs. |

| Single earner + parents + child (school) | 67% | 8% | 25% | Wants take the hit. Savings stay protected. |

| Single earner + parents + child (college approaching) | 68% | 7% | 25% | Redirect SIP to education goal. Reduce other wants. |

| Near retirement, no dependents | 48% | 17% | 35% | Maximise NPS, PPF, and equity SIPs. |

The 25% savings target is held constant across all life stages deliberately. The variable is always the wants bucket, not the savings bucket. This is the core discipline of adapted budgeting.

How to Actually Implement the Adapted 50/30/20 Rule

Knowing the percentages is the easy part. Implementing them in a real household with shared bank accounts, informal cash flows, and unpredictable family needs is harder. Here is a practical approach.

Step 1: Calculate Your Real Take-Home Income

Use your net in-hand salary, not CTC. Deduct EPF contributions, professional tax, and any other automatic deductions. This is your true budgeting base.

Step 2: List Every Shared Obligation First

Before you categorise anything, list every recurring obligation that involves another family member. Parent transfer, school fees, insurance premiums for parents, any shared loan. These are fixed needs. Non-negotiable.

Step 3: Set Up Automated SIPs Before the Month Begins

Set your SIP date to the 2nd or 3rd of the month, right after salary credit. This forces your budget to work around the savings, not the other way around.

Step 4: Track Net Worth, Not Just Monthly Spend

Monthly budget tracking tells you where money went. Net worth tracking tells you whether you are actually building wealth. Track your FDs, SIPs, EPF, PPF, and real estate value together. See the complete family financial picture in one place.

Step 5: Review the Allocation Every 6 Months

Family obligations change. A parent’s medical condition may worsen. A child advances to a higher fee bracket. Income may grow. Revisit the allocation every six months and adjust accordingly.

How Famli Helps Single Earners See the Full Family Financial Picture

Implementing an adapted budgeting rule is much easier when you can see your entire family’s financial position in one place. That is exactly what Famli is built for.

- Track all family assets together: SIPs, FDs, EPF, PPF, LIC, and real estate in a unified net worth dashboard

- Invite your spouse or parents to see a shared financial view. No more running numbers alone.

- Set and track shared financial goals, including your child’s education corpus and parent emergency fund

- Get guidance from Buddy, Famli’s in-app AI assistant, on understanding your financial position

- Connect via the RBI-regulated Account Aggregator framework for secure, consent-based data fetching

Famli does not manage your money or make investment decisions for you. It gives your family the visibility and clarity to make informed decisions together.

Famli is a SEBI-registered Investment Adviser (IINA000021979) and ISO 27001 certified.

Frequently Asked Questions

Does the 50/30/20 rule work for Indian families?

The standard 50/30/20 rule works as a starting framework but needs significant adaptation for Indian families. The needs bucket typically expands to 60 to 67% when joint family obligations, aging parent support, and children’s education are factored in. The wants bucket shrinks to accommodate this, while the 20% savings target should be protected as a floor.

How do I budget for aging parents in India?

Include a fixed monthly parent transfer in your needs bucket and treat it like an EMI. Additionally, build a separate parent medical emergency corpus of Rs 50,000 to Rs 1,00,000 that you do not use for anything else. Factor in parents’ health insurance premiums, which for senior citizens can run Rs 18,000 to Rs 36,000 per year.

Should children’s education be in needs or savings?

Current education costs (school fees, tuition, transport) belong in the needs bucket. Future education costs (building a corpus for college or professional courses) belong in the savings bucket as a dedicated SIP goal. Both are non-negotiable. Do not sacrifice either to maintain lifestyle wants.

How much should a single earner save per month in India?

The floor is 20% of take-home income. For a single earner supporting a joint family, this may feel difficult, but it is achievable with disciplined budgeting. Prioritise automating SIPs so savings happen before spending. If your obligations are temporarily very high, maintain a minimum savings rate of 10% and build back to 20% as income grows.

What is the best way to track family finances in India?

Use a single consolidated view of all family assets, including SIPs, FDs, EPF, PPF, LIC, and real estate. Tools like Famli allow families to aggregate this data in one place using the RBI-regulated Account Aggregator framework, giving every family member visibility into the shared financial position.

Can SIP be used as the primary savings vehicle for Indian families?

Yes. SIPs (Systematic Investment Plans) in mutual funds are one of the most effective long-term savings vehicles for Indian families. They automate savings discipline, allow small monthly contributions, and benefit from rupee cost averaging over long investment horizons. For education and retirement goals specifically, a long-horizon equity SIP combined with PPF or NPS forms a strong foundation.

| Track Your Family’s Financial Health with Famli See your FDs, EPF, Cards and more in one unified dashboard. Set shared goals. Get clarity together. Download Famli from the App Store or Google Play. SEBI-registered Investment Adviser |

Disclaimer: Investments are subject to market risks. Famli is a SEBI-registered Investment Adviser (INA000021979). Registration does not guarantee performance of advice or assurance of returns. Please read all scheme related documents carefully before investing. The figures used in this article are illustrative and for educational purposes only.