What Is Mutual Fund Overlap? (And Why It Matters More Than You Think)

Mutual fund overlap occurs when two or more funds in your portfolio hold a significant percentage of the same underlying stocks or securities. In practical terms: you may be investing in five different mutual funds every month, but a large portion of your money is effectively buying the same 10 to 15 companies, repeatedly, across every one of those funds. The funds may carry different names, different fund house branding, and different NAVs, but under the hood, they may have almost identical composition.

This is not a fringe problem. It is one of the most common and least-discussed inefficiencies in Indian household portfolios today.

The Over-Diversification Trap

There is a widely held belief that more funds equal more diversification. It is an intuitive assumption, and it is largely wrong.

True diversification means spreading risk across assets that do not move in the same direction at the same time: different asset classes, different sectors, different market caps, different geographies. What most Indian families end up with is something different: multiple large-cap funds, multiple flexi-cap funds, and multiple multi-cap funds, all of which are legally required to hold a substantial allocation to the same top 100 NSE-listed companies.

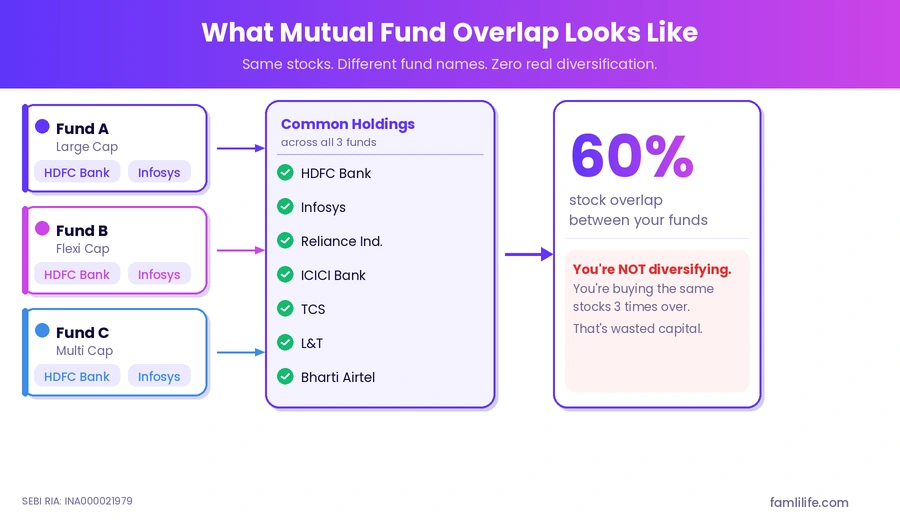

A study of the top 10 most popular mutual funds in India by SIP volume consistently shows that the top 20 to 25 stock holdings repeat across nearly all of them. HDFC Bank, Infosys, ICICI Bank, Reliance Industries, and a handful of other blue-chips appear in virtually every large-cap and flexi-cap portfolio. If your family holds three such funds, you are buying these names three times over, under the illusion of diversification. This is the over-diversified mutual fund portfolio trap: the appearance of breadth with none of its benefits.

Why Indian Families Are Particularly Vulnerable

The structure of how Indian families accumulate mutual funds creates a natural path toward portfolio overlap.

Most families do not build a portfolio in one sitting. A SIP gets started on the advice of a friend. Another gets started when a bank relationship manager calls. A third comes from a workplace investment platform. A fourth is opened by a spouse, independently. Over three to five years, a household can end up with eight to twelve active SIPs, opened at different times, on different platforms, with no single view of the full picture.

This is not a failure of financial awareness. It is a structural gap: most people simply do not have a tool that shows their family’s complete mutual fund portfolio in one place, across all accounts, for all family members together.

The result is a common pattern: too many SIPs in the portfolio, high monthly outflow, significant duplication across funds, and no clarity on whether the family is actually spreading risk or just spreading paperwork.

How Overlap Quietly Works Against You

Mutual fund overlap in a family portfolio creates three specific, measurable problems.

Concentration risk masquerading as diversification. If 60% of your total mutual fund corpus is indirectly allocated to the same 15 stocks, you carry the same downside risk as a concentrated portfolio, without the intentionality that comes with one.

Harder to rebalance with clarity. When multiple funds hold the same stocks, your actual asset allocation becomes impossible to read accurately. You may think you have 60% in equity and 40% in debt, but within your equity allocation, you are unknowingly overweight a handful of sectors like banking and IT simply because every large-cap fund you hold gravitates toward the same top stocks. When markets move and you want to rebalance, you cannot do it cleanly because you do not have a true picture of what you actually hold underneath the fund names.

Capital inefficiency. Every additional overlapping fund adds zero new diversification benefit. The SIP amount going into a fourth large-cap fund could instead be going into a completely different asset class, a debt instrument, or a truly distinct equity category. Overlap is, in effect, a misallocation of monthly investments.

Research from various online tools points to a practical threshold: for most retail Indian investors, a well-structured mutual fund portfolio requires no more than four to six funds, provided those funds are genuinely distinct in mandate, market cap category, and underlying holdings.

Signs Your Family’s Portfolio Has Too Much Overlap

Before running a full mutual fund overlap analysis, these are the warning signs to look for:

- You hold more than two funds in the same category (for example, two large-cap funds or two flexi-cap funds from different fund houses)

- Your portfolio has six or more active SIPs with no documented rationale for each one

- You and your spouse have separate investment accounts with no shared view of combined holdings

- You opened one or more SIPs in the last two years without reviewing whether the mandate overlaps with existing funds

- You cannot name the top five stocks held across your combined portfolio from memory

- Your portfolio review, if you do one at all, happens fund by fund rather than at a consolidated family level

If three or more of these apply, there is a meaningful probability that mutual fund duplication is already affecting your family’s portfolio.

The Portfolio Consolidation Checklist: How to Fix a Messy Portfolio

Consolidating a portfolio with significant overlap is a structured process, not a panic sell. Here is a step-by-step checklist for how to approach mutual fund portfolio consolidation in India:

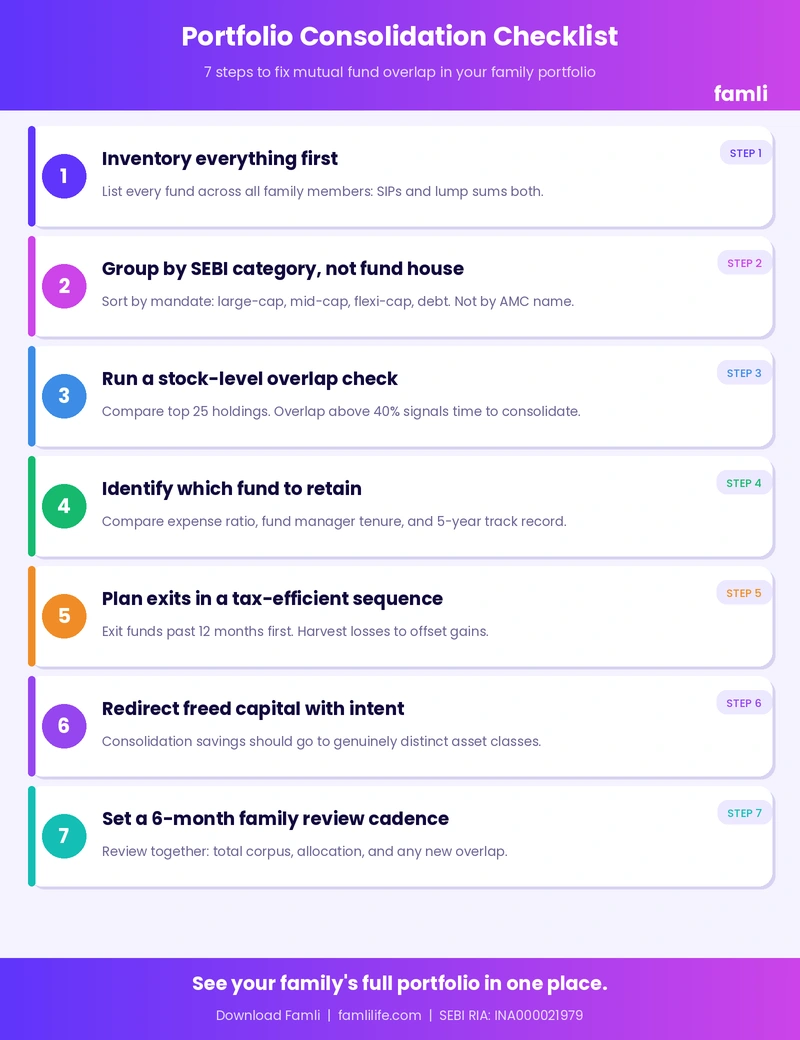

Step 1: Inventory everything first

- List every mutual fund held across all family members: spouse, parents, adult children

- Include both SIPs (ongoing) and lump sum investments

- Note the fund category for each: large-cap, mid-cap, small-cap, flexi-cap, ELSS, hybrid, debt, etc.

- Do not make any redemption decision until the full picture is in front of you

Step 2: Group by category, not by fund house

- Sort all funds by SEBI-mandated category, not by the AMC name

- Identify how many funds you hold in each category

- Flag any category where you hold more than one fund (this is the first layer of overlap)

Step 3: Run a stock-level overlap check

- For each pair of equity funds, compare the top 20 to 25 stock holdings

- Calculate the approximate overlap percentage: if 15 of the top 25 stocks are common between two funds, overlap is approximately 60%

- Overlap above 40% between two funds of the same category is a strong signal to consolidate

- Several free tools in India allow this analysis.

Step 4: Identify the fund to retain in each category

- Compare expense ratios, fund manager tenure, 5-year and 10-year CAGR (for context, not prediction), and AUM stability

- Retain the fund with the stronger track record and lower cost

- If both funds are in an ELSS category, check the lock-in period before any decision

Step 5: Plan exits in a tax-efficient sequence

- Equity funds held for less than 12 months attract short-term capital gains (STCG) tax at 20% (post Budget 2024)

- Equity funds held for more than 12 months attract long-term capital gains (LTCG) tax at 12.5% on gains above Rs. 1.25 lakh per year

- Prioritise exiting funds that have crossed the 12-month mark, or funds that are sitting at a loss (harvesting tax losses to offset gains elsewhere)

- Stop SIP contributions into the overlapping fund immediately, even before redemption, to prevent further capital allocation to a redundant position

Step 6: Redirect capital with intent

- Before moving capital, define what the consolidated portfolio should look like

- A commonly recommended structure for Indian families: one large-cap index fund, one mid-cap or small-cap active fund, one flexi-cap fund for core equity, and one debt fund for stability

- Any surplus SIP capacity freed up by consolidation should go into genuinely distinct categories: PPF, NPS, or a short-duration debt fund, depending on the family’s liquidity needs and time horizon

Step 7: Set a review cadence and stick to it

- Commit to a portfolio review every six months at the family level, not just individually

- Review should cover: total corpus, asset allocation, SIP amounts, and whether any new overlap has been introduced

- Treat it as a family financial conversation, not a solo exercise

The Family Dimension: Why You Cannot Fix Overlap Individually

Here is the part that most portfolio consolidation guides miss entirely.

Mutual fund overlap in Indian families is not just an individual problem. It is a household problem. A wife may hold a flexi-cap SIP. Her husband may hold a different flexi-cap SIP. Her father-in-law may hold a large-cap fund that effectively mirrors both. No one person looking at only their own account would ever see the full extent of the overlap.

Getting a clear picture of your family’s full mutual fund holdings is the first step. Once every fund across every family member is visible in one place, category-level duplication becomes immediately apparent without needing a separate tool.

This is why family-level visibility is not a nice-to-have feature. It is the prerequisite for making any consolidation decision accurately. Without a consolidated family view of all mutual fund holdings, you are solving an incomplete version of the problem.

How Famli Helps You See the Full Picture

Famli is built specifically for this problem. As a SEBI-registered Investment Adviser (INA000021979), Famli gives your family a single dashboard to track every asset across all accounts and all family members: SIPs, lump sum mutual fund holdings, FDs, LIC, EPF, NPS, and more.

When your family’s full mutual fund portfolio is visible in one place, patterns that were invisible become obvious: the duplicate large-cap SIPs, the three flexi-cap funds with nearly identical holdings, the overall equity-to-debt split that no individual account reveals.

Famli is built so that you can identify such gaps and opportunities in your journey towards building family wealth. It gives you the clarity to see what you already hold, across your entire family, so that decisions like consolidation are based on the complete picture, not a partial one.

Start by getting a full view of your family’s portfolio. Download Famli and connect your accounts in minutes.

Frequently Asked Questions

Q: What is mutual fund overlap?

A: Mutual fund overlap occurs when two or more funds in your portfolio hold a significant percentage of the same underlying stocks. You may be investing in five different funds but a large portion of your money is buying the same 10 to 15 companies across all of them.

Q: How much mutual fund overlap is acceptable?

A: Overlap above 40% between two funds in the same category is a strong signal to consolidate. For most Indian retail investors, a well-structured portfolio needs no more than four to six funds that are genuinely distinct in mandate and underlying holdings.

Q: How do I check mutual fund overlap in my portfolio?

A: Compare the top 25 stock holdings between each pair of funds you hold. Calculate what percentage of stocks are common. Famli – the privacy-first family wealth management app allows side by side comparison of fund holdings.

Q: How many mutual funds should an Indian family have?

A: Research suggests four to six funds is optimal for most Indian retail investors, provided those funds are genuinely distinct in category, market cap focus, and underlying holdings. More than six funds in the same categories typically creates overlap without adding diversification.

Q: What is the difference between over-diversification and diversification?

A: True diversification spreads risk across assets that do not move in the same direction: different asset classes, sectors, market caps, and geographies. Over-diversification is holding multiple funds that are superficially different but hold the same underlying stocks, creating an illusion of breadth with none of its benefits.

Disclaimer: Investment in securities market are subject to market risk, read all related documents carefully before investing. Registration granted by SEBI, enlistment as IA with Exchange and certification from National Institute of Securities Markets (NISM) in no way guarantee performance of the intermediary or provide any assurance of returns to investors. Famli is a SEBI-registered Investment Adviser (INA000021979).The information in this article is for educational purposes only and does not constitute investment advice.